VC's and the Faith + Tech Market

How venture capital thinks about the emerging opportunities for faith-driven technology.

Hey friends, welcome to the Missional Labs Journal. This newsletter is for church and ministry leaders interested in the macro-trends (innovation, tech, culture, etc) shaping our world, and the implications for entrepreneurial missional leadership.

Today’s newsletter is a guest post from my friend Grant Demeter, a VC at The Yard Ventures, a thoughtful Christian in my community, and an all-around good guy.

Grant helps us understand the market for faith-driven technology ventures in North America, and clues us in to what venture capital is most interested in right now. It’s still early - but there are some serious investments picking up speed from Silicon Valley.

These trends are important for the Church at large to understand . I think integrating good missiology, Christian spirituality, and wise entrepreneurship is the best way to pioneer a new future for the Church in modern culture. This means understanding these trends is essential - that’s what Grant helps us do.

Don’t miss some of Grant’s previous related articles here and here.

Let me know what you think, subscribe, and share!

Tyler

Hello and welcome back to Markets by Grant — the final piece in my series about startups’ journey to the center of the consumer’s private life. Rather than reiterating my thesis on the space (again), I’ll have Connie Chan of a16z do it for me:

“One thing that I’ve always thought deeply about is how do I find investments that are tied to what people deem to be a core part of their identity. When you look at these communities that people strongly identify with, that’s where they spend most of their time. That’s where you get longer-term retention.”

Well said.

Before I dive in, a quick note:

I understand that using venture lingo to analyze religious “users” is sensitive territory for many. Sorry in advance for that. There’s understandable discomfort in allowing tech to penetrate these sacred parts of our lives which many feel are better left in their essential forms. For what it’s worth, I don’t believe that tech-enabled solutions cheapen religious practice, and I also don’t believe that religious people are as simple as consumers, customers, or end users.

The Dollars

Sizing the religion market in terms of dollars is a big, nebulous task, which I’m not going to spend too much time on. Like with GDP, it’s tough to not double-count, and also like with GDP, many market size estimates include multipliers for the estimated downstream impact of religious organizations. A recent, comprehensive study sized the U.S. Market at $1.2B using this approach.

I’ve shaved down this broad estimate to what I view as a more conservative market definition:

While before, the market size was almost certainly overcounted, I now believe it to be undercounted — as it doesn’t value the use of preexisting media and technology to facilitate religious activities — ie: Zoom for worship, Facebook for events, Venmo for tithing, etc. Of note, I’ve also excluded charitable organizations, many of which are operated by and for religious organizations.

For those who read my last piece on the global religion market, I’ll quickly acknowledge the reader whiplash from moving from a global perspective down to a US-only perspective. Other studies (which also happen to estimate the US market at $130B in 2022), have sized the global market at about $360B.

Most estimate the CAGR at between 5 and 7% (I’ve used 5% in my estimation). What’s driving it? Digitization and virtualization, according to most sources. More on that later.

And quickly, a chart of VC funding to validate that I’m not the only VC investor starting to think this might be a favorable market:

Funding is taking off…although the comparatively small dollar amounts indicate we’re still early to the game.

And what is the game? What kind of startups are out there? And what are they replacing/enhancing?

The Landscape

This whole writing series has been on consumer-facing startups, but I think the B2B angle (ie: selling into churches, mosques, etc) in this market is too fascinating to skip, so I’ll touch on it as well. Here’s how I think about the layout of this market:

The Protestant Christian tradition actually has a very interesting framework for categorizing religious organizations. Simply put, religious organizations are either Modalities or Sodalities.

Modalities are organized communities of faith: churches, mosques, temples, etc — which operate core, internal religious operations for their communities (services, ceremonies, etc). Modalities are largely pass-through, democratized entities. All funding effectively originates from the religious consumer, who is a congregant of a given modality, and is routed toward core operations or toward Sodalities…

Sodalities are para-organizational — they operate across or above multiple communities of faith as service providers. They are charities, missions, consultancies, agencies, software companies, and every other organization which serves the religious adherent or modality. Sodalities’ revenues either come from modalities (B2B), or directly from religious consumers (B2C).

Long story short — from here on out, we’re talking about for-profit sodalities. In other words, I’m not going to opine on the valuation or exit likelihood of Mosque A or Church B. Instead, I’ll discuss FaithTech startups which help faith-based modalities (organizations) or individuals operate their religious lives.

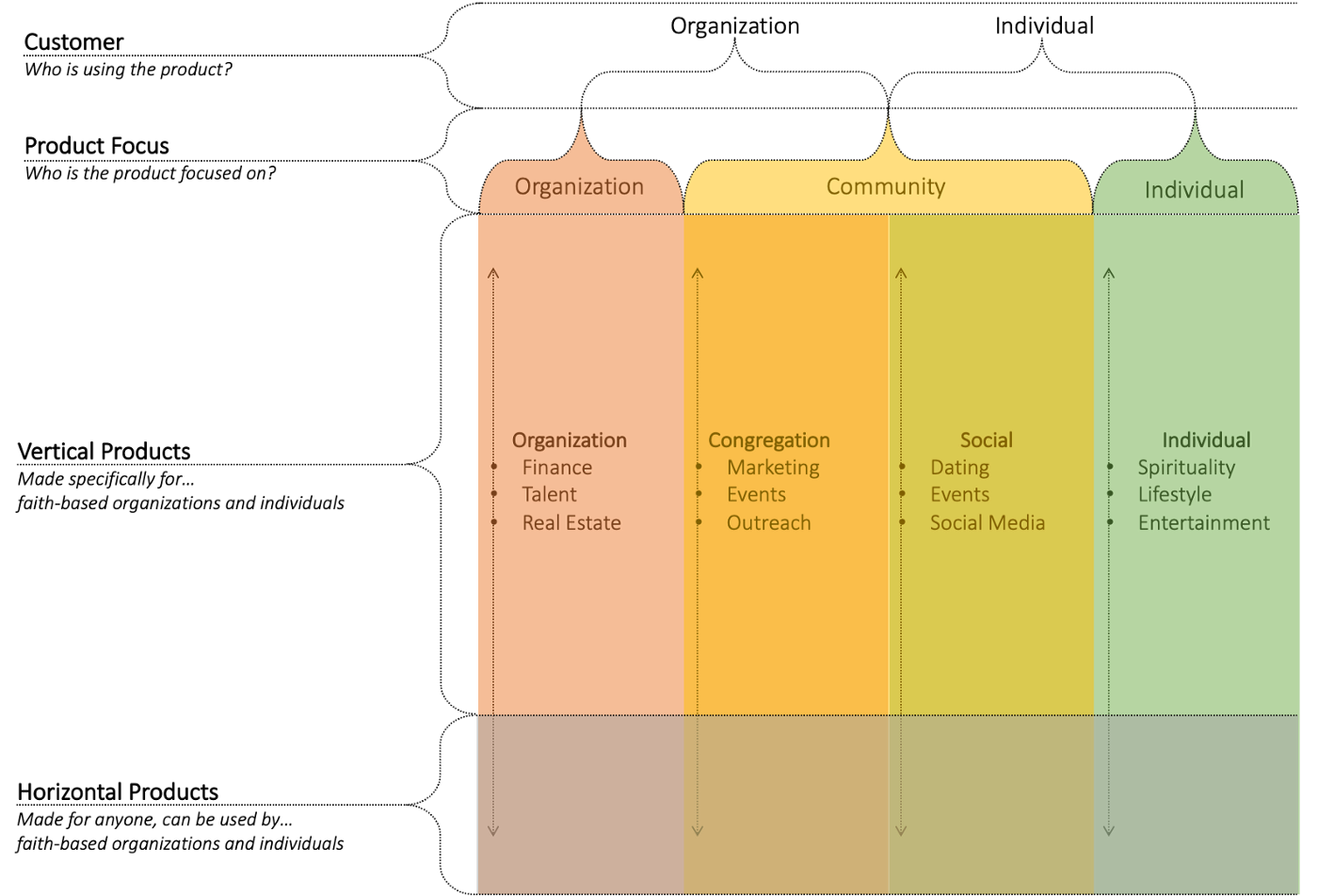

With all this in mind, here’s how I’d visualize the market:

To sum up my graphic, as a FaithTech startup, you can target organizations (churches, synagogues, mosques, other communities of worship) or individuals of faith. Ie: B2B or B2C. And I’d break it out one level further. For your target customer, your product or service will either be focused internally or externally on their faith community.

This breakout brings us to four categories of products in the space:

Organization: Products used by faith-based organizations, for faith-based organizations.

In this bucket, we see classic “keep the lights on” solutions–like payroll, HR, finance, procurement, etcCongregation: Products used by faith-based organizations, to engage with their communities.

In this bucket, we see the equivalent of CRM, marketing, outreach, events platforms, communication infrastructure, etcSocial: Products used by faith-based individuals, to engage with their communities.

Here’s where we see the dating apps and the social media sitesIndividual: Products used by faith-based individuals, for faith-based individuals.

And here’s where I’d bucket the prayer apps, foodtech, media and entertainment, fashion, and other consumer-y stuff

…And then there’s that “Horizontal Products” bar at the bottom. This brings us to a key question: do we really need tech purpose-built for organizations or individuals of faith? Or can they get on just as well with existing available products?

Before we answer that question, let’s break down some of the players in the space:

Wow, what a beaut. Lots to discuss. First, a brief orientation.

Of the spaces I’ve looked into, FaithTech has the least number of venture-funded startups. There are just a handful, and they’re pretty much all on the right hand side of my market map. To build up the suspense, I’ll move left to right as I add a bit of color to what I’m seeing in each of these spaces.

B2B

Vertical SaaS: 👍

This space is almost entirely dominated by small mom-and-pop software providers who have been around since the 90’s. Most of them provide basic ERP-style finance and HR capabilities, plus congregation management solutions which focus on scheduling, donor management, communications and engagement, and services and events. Not all provide all, but most provide some.

There’s little to no venture capital activity over here, but there’s still a lot going on. Five to ten years ago, someone caught wind that these unassuming vertical SaaS providers were printing money in their overlooked profitable niche. Since then, there’s been significant rollup activity. Ministry Brands, as an example, has been on a quiet acquisition spree in the space for the past decade. It now owns 30+ FaithTech businesses, serves 95,000+ faith-based organizations, and has $100M+ in EBITDA. In 2016, it was acquired for $1.4B by Insight Partners, and was spun out in November for an undisclosed amount (rumored to be around $4B).

I would actually find this to be a very promising space for a startup to enter and disrupt. The market, even if not growing at breakneck speed, is giant. And it’s a classic disruption scenario: customers are currently using old-school solutions, which haven’t had incentive to improve due to lack of competition. Rollups like Ministry Brands generate enterprise value with an acquisition and scale strategy, not an innovation strategy. I would love to see an innovative consumerized vertical SaaS startup enter with the vision of taking organizational FaithTech into the 21st century — taking this sleepy market by storm and winning a big acquisition from Ministry Brands or otherwise.

Conversion and Evangelism:❓

Gloo has seen a lot of press for its practices of scraping social media for signals of ‘convertibility’ (for lack of a better word). The software identifies individuals in a religious organization’s reach who are either expressing openness to religion (through posts and click patterns), or are exhibiting signs of vulnerability following significant life events (ie: divorce, unemployment, etc). Both categories signal that they may be more receptive to and impacted by religious outreach. Gloo then flags their profiles for targeted marketing/advertising/outreach by the religious organizations. Some view it as very altruistic, missional work, others view it as a violation of sensitive private data (a la Cambridge Analytica). I don’t have a point of view, but it’s regardless fascinating.

Virtual Events and Services, Communications and Community Engagement: 👎

This space is rumored to be driving much of the growth in the B2B side of this market, thanks to virtualization trends driven by COVID. The problem is, religious organizations need more than a video live streaming solution or a congregation communications platform. They need to be onboarded to a fully integrated digital system, built for their operational rhythms. Thus, the software play has been less successful than the professional services play — ie: agencies and consultancies building new integrated websites, tools, and strategies for organizations, one by one. There’s no doubt that this is a critically important growth factor for the future of religious organizations — I just don’t think that the buyer sophistication is there yet to support a scalable software market.

A quick aside: An interesting side effect of the move to virtualization of religious services is consolidation of religious organizations. For churches in particular, laggards to adopt hybrid solutions have seen their congregations shrink, or have been ‘acquired’ by larger, more tech-native church conglomerates. Interesting stuff.

But what about virtual-first modalities who exist primarily in the metaverse? Platforms like SoWork, AltospaceVR, and others are starting to be used not just as avatar-led office/hangout/event space, but as the definitive meta-home for houses of worship. Life.Church is a prominent example of a metaverse-first church, and other upstart churches are finding it easier and more scalable to start off virtually.

Ask Bradley Tusk of Tusk Ventures: “Why spend the money building something, raising funds, and getting permits, when you can hire a really good Web3 developer, build your church in the metaverse, and it’ll probably grow a lot faster.”

While I agree that this may work for new modalities, I don’t think this shift is so easy for established communities. And again, I’m not the only one to recognize the importance here. Meta/Facebook is on the case. The behemoth is in the midst of a significant, multi-year effort to be the future home of religious organizations, and is building a suite of paid tools to enable them to operate, host events and services, and cultivate their communities — all on Facebook’s metaverse. They’ve partnered with renowned megachurch Hillsong for development and testing efforts, among others. Notably, Sheryl Sandberg has stated that religious organizations are the “best of Facebook”, and indicates that they are “a natural fit because fundamentally both are about connection.” An empty, sales-y, overly high-level statement, but one which belies the importance of the initiative to Meta.

Before we move on to my analysis of the consumer innovation areas, one quick business idea. This is a giant market, and we want the software play to work, but there’s a lack of buyer sophistication which creates softness on the supply side. Meanwhile, leaders of faith-based organizations tend to be more resistant to traditional commercial sales motions, compared with today’s business buyer. That puts us in a tough spot.

It’s not fully fleshed out, but I’m interested in the idea of a layer which connects modalities with tech-enabled sodalities. It’s a blended vertical B2B search engine, marketplace, and content company, which sits closer to modalities than a software startup, with a gentler sales conversion journey. The idea is to be the definitive place/portal for leaders/administrators of faith-based organizations to engage with technology to support operations and objectives. Ie: learn about tech, see how other modalities are using it, find software/service providers, engage with them, etc.

Anyway, it’s a work in progress. If you think it’s a dumb idea, whatever, I barely put any thought into it. If you think it’s a great idea, thank you so much! I spent a lot of time thinking it through!

Consumer

Social Media, AKA Faithbook: 👎

In a reaction to Facebook’s dominance as well as its secularism and data politics, many have tried to create the Facebook equivalent for faith-based individuals. These efforts have seen limited success, and I don’t see this verticalization as a compelling strategy. Network effects of these platforms are negative from the start given Facebook’s looming presence. How dominant is Facebook? Well, Facebook has ~3 billion monthly active users, making it larger than Christianity worldwide (2.3 billion), or Islam (1.8 billion). Yikes.

‘Faithbook’ is a filter, not a product. And as it happens, it’s also a giant Facebook group. Point made. And to hammer it home, Facebook is making a concerted effort to attract and retain more religious users, to complement its courtship of religious organizations. Good luck to anyone trying to compete with that.

Dating Apps: 👎

While new entrants always seem to be popping up (see: the elite Jewish dating community, Lox Club), the bulk have been around for quite some time. Meanwhile, most horizontal dating apps have religion filters, and most users use more than one app. The burden of differentiation for creating a new religious dating app in this already-crowded market is very high, and I doubt that it would make sense.

Prayer and Meditation, and Engagement with Holy Texts: 👍

Here is where the VC money has been lately. These startups build content around religious texts, beliefs, and practices for religious consumers to engage with. Some lean toward meditation/relaxation, and others lean toward traditional prayer practices — but they all create and monetize their own content. I feel this is one of the more defensible strategies in the space. It creates stickiness by elevating religious text engagement with structured content, while providing some of the emotional/affective benefits of meditation, relaxation, and routine. Meanwhile, there is a strong precedent for this type of daily practice in most religious traditions.

Again, Connie Chan says it well:

“The market for these apps is still largely untapped. The YouVersion Bible app has logged more than 500 million downloads. It’s a nonprofit, but if that app was a for-profit company, it would have been a unicorn many times over long ago. Consumers have always been using these apps, but investors are now starting to realize some for-profit companies are being formed that are also delivering great experiences.”

Interesting stuff. The business model and product concept do seem kind of ten-years-ago (ie: we’re investing in consumer apps again?), but the traction has been strong enough and the market is large enough to reasonably generate multiple multi-billion dollar exits.

FinTech and Commerce -❓

In Fintech, we’re largely seeing Muslim-focused consumer investing apps which filter investment opportunities based on Sharia Law. The product versus filter question might come to mind, but even if another consumer investing platform (RobinHood, OpenSea) had filters for Sharia-compliant opportunities, it’s possible that adherent faith-based investors might still prefer to avoid supporting a business which profits from non-Sharia investments as well. One might then ask the question of how big the market for Sharia-adherent consumer investors is, and I confess that I’m not sure (inexcusable laziness). Beyond Sharia, I’m seeing a lot of values-based investing platforms as of late, and the market hasn’t settled enough to indicate the promise of these business models (more laziness on my part).

The same applies for Halal and Kosher foodtech. I could be missing something obvious, but I haven’t seen Halal/Kosher-specific BlueApron-equivalent meal kit delivery startups. Many offer Halal or Kosher options, but can’t guarantee their facilities as such. Would there be enough scale in these markets to make the unit economics work, where they haven’t before?

Lastly, modest fashion, religious media/entertainment, religious tourism, and child-focused religious EdTech are four more spaces under this umbrella where I’m seeing promising activity…but oh wow — look at the time! I think I’d better leave it here.

Thanks for sticking with me — I’d welcome any feedback, thoughts, or ideas. I’ll be monitoring this space closely, and if any interesting startups come your way, send them over!

— G